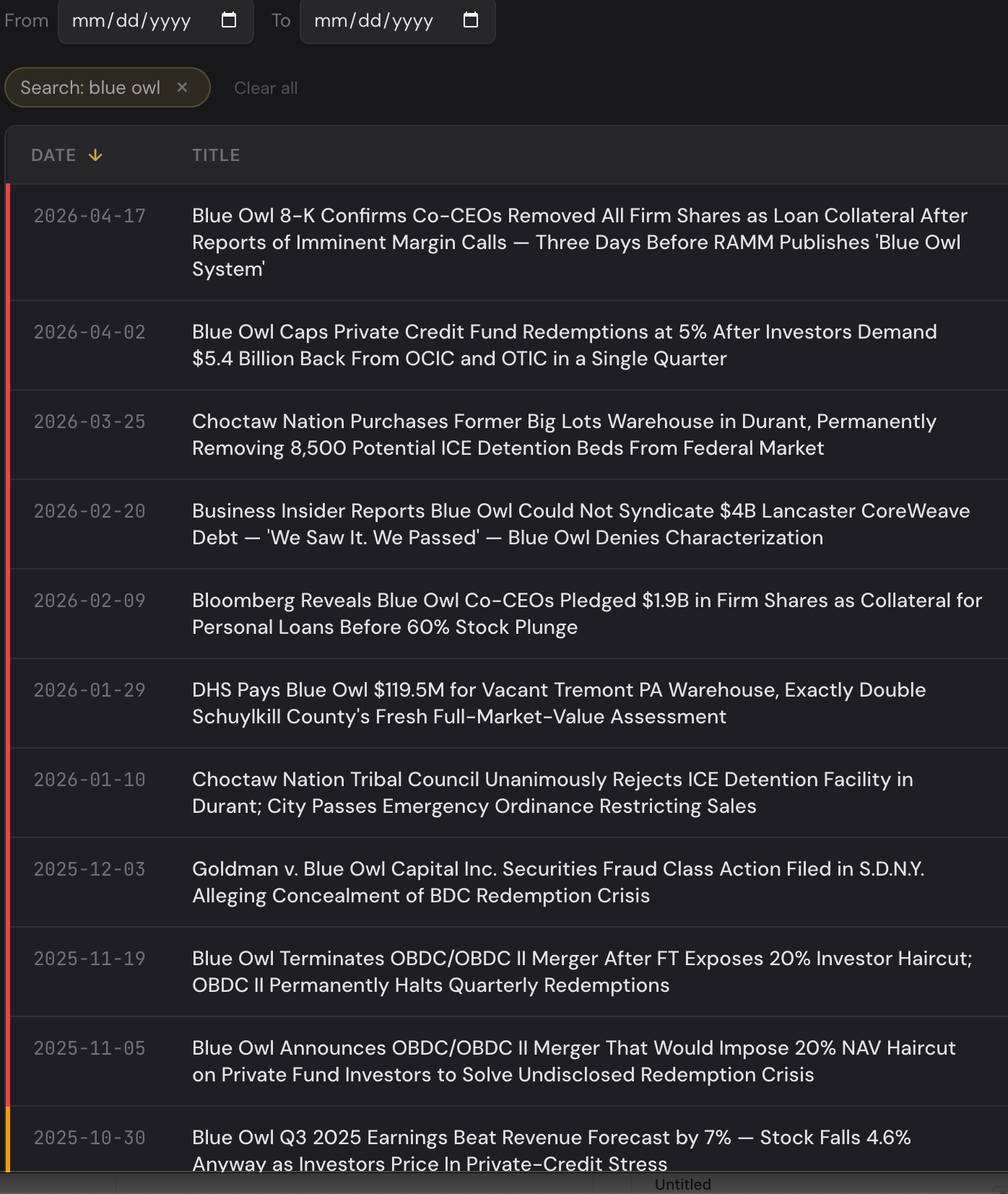

The Blue Owl System: The $119.5 Million Rescue

Blue Owl Capital was hemorrhaging cash when DHS paid $119.5 million for its vacant Pennsylvania warehouse — exactly double the county's fresh assessment.

Days before this piece was published, Blue Owl Capital’s co-founders quietly removed roughly $1.1 billion in firm shares from the collateral behind their personal loans. Bloomberg reported the filing was driven by concerns about imminent margin calls. The stock had fallen more than 60 percent from its 52-week high. A federal securities fraud class action was already pending, alleging Blue Owl had concealed this liquidity crisis from the public.

Two months earlier, on January 29, 2026, a Delaware LLC called BIGTRPA001 — a subsidiary of Blue Owl Real Estate Net Lease Property Fund — transferred a vacant 1.3-million-square-foot warehouse in Tremont Township, Pennsylvania, to the United States of America. The county’s Chief Assessor had certified the property’s value at $59,600,000 ten weeks earlier as part of Schuylkill County’s first comprehensive reassessment since 1996. Under the predetermined ratio that Schuylkill County commissioners adopted in May 2025, that figure is not a fraction of anything — it is 100 percent of full fair market value as of January 1, 2025. The Department of Homeland Security paid $119,515,000 — exactly double market value.

Thirty-three Trump administration officials held Blue Owl stock, funds, or carry interests at the time of the transaction. Among them: the President of the United States, the Secretary of the Navy (whose department administers the procurement vehicle that moved the money), the Assistant Secretary of the Navy responsible for installations (sworn in five weeks before the deed took effect, still holding OWL shares directly), the Comptroller of the Currency (who holds the specific Blue Owl real estate vehicle), and twenty-nine others across thirteen agencies. Some have divested. Some still hold. None has publicly recused from WEXMAC-TITUS matters.

This is what separates the Blue Owl transaction from the ten others in the WEXMAC-TITUS detention buildout. Deutsche Bank sold an inflated asset. PNK Group flipped speculative construction at a 333 percent markup. Rockefeller Group held a $12 million property for three years and sold it for $70 million. Those were corrupt sales — institutional sellers extracting value from a captured government. The Blue Owl transaction was something else. The seller was in acute distress. The buyer paid rescue prices. The beneficiaries were the firm’s shareholders, which included the President and the senior civilian responsible for Navy installations.

This wasn’t a sale. It was a rescue — and the point of a captured network is not that anyone had to decide to rescue Blue Owl. The point is that a network configured this way had no incentive to let the firm fall.

Tremont Township has approximately 300 residents. Its annual loss in property tax revenue, now that the federal government holds the deed and federal property is tax-exempt, is approximately $1 million. The Pine Grove Area School District loses roughly half of its expected annual revenue increase from the reassessment — a single parcel erasing roughly fifty cents of every new dollar the reassessment was projected to produce for local schools. County commissioners learned of the sale when the deed was recorded. ICE has since told local press it projects 7,500 beds for the site — which would make Tremont one of the three largest immigration detention facilities in the country.

Two hundred miles south of Tremont, the Choctaw Nation saw the same trade coming and stopped it. More on that below.

The RAMM documents the connections that beat reporting can’t see — 4,776+ sourced events at capturecascade.org.

Free subscribers get every investigation. Paid subscribers get draft chapters of the book and access to the research infrastructure.

The chain of title

The Tremont warehouse arrived at Blue Owl through four transactions across six years.

In 2020, Big Lots entered a $725 million sale-leaseback agreement with Oak Street Real Estate Capital covering all four of its major distribution centers: Columbus, Ohio; Montgomery, Alabama; Tremont, Pennsylvania; and Durant, Oklahoma. The Tremont and Durant properties were each approximately 1.3 million square feet. Big Lots continued occupying the facilities as a tenant under long-term net leases. Net proceeds to Big Lots were approximately $550 million, used to pay down its revolving credit facility.

In 2021, Blue Owl Capital acquired Oak Street Real Estate Capital for $950 million. The entire Big Lots portfolio passed to Blue Owl Real Estate Net Lease Property Fund — held through a Delaware LLC designated BIGTRPA001 for Tremont, with a corresponding vehicle for Durant.

In 2024, Big Lots filed for bankruptcy. It closed the Tremont distribution center in December, laying off 505 employees. It closed Durant around the same time. Blue Owl now held vacant 1.3-million-square-foot warehouses in rural Pennsylvania and southeastern Oklahoma — with no tenants, no income, and a private credit market entering acute distress.

In January 2026, the Department of Homeland Security agreed to purchase Tremont. The deed was signed January 15 and took effect January 29. Purchase price: $119,515,000.

ICE was also moving to acquire Durant. The Choctaw Nation stopped them.

Durant, Oklahoma: The Control Case

The Choctaw Nation’s tribal headquarters sits approximately 1,000 feet from the Durant warehouse. Adjacent to the site are Choctaw Nation childcare facilities and elderly services offices. On January 10, 2026, the Choctaw Nation Tribal Council passed a unanimous resolution opposing any ICE detention facility at the location. Council member Regina Mabray called the site “unacceptably close to the nation’s governmental headquarters.” That same day, the Durant City Council passed an emergency ordinance making it illegal to operate a detention center within city limits without a conditional use permit.

In late March 2026, the Choctaw Nation purchased the warehouse outright. Chief Gary Batton announced the acquisition as supporting operational growth adjacent to tribal headquarters. The price was not disclosed. The property was removed from the federal market entirely. Project Salt Box, the volunteer research organization that has been tracking the ICE warehouse program, estimated the purchase foreclosed approximately 8,500 potential detention beds from ICE’s pipeline.

Durant is the control case for Tremont. Same portfolio. Same federal interest. Same stranded-asset pressure on Blue Owl. The difference was that one community had a sovereign institution with the legal capacity and the political will to intervene before the federal transaction could close.

Pennsylvania had no Choctaw Nation. Schuylkill County’s commissioners learned about the Tremont sale from the recorded deed.

A firm in acute distress

To understand why the Tremont transaction was a rescue, look at the seller at the moment of sale.

Blue Owl Capital (NYSE: OWL) peaked at a 52-week high of $25.89 in 2024. As the Tremont deed was being finalized in January 2026, the stock was trading in the low teens. On April 17, 2026, it closed at $9.80, down more than 60 percent from peak. Zacks assigns the stock a #5 rating, Strong Sell. Barclays has cut its price target to $9. Goldman Sachs — itself a counterparty to Blue Owl on multiple other warehouse transactions in the same program — cut its target to $14 and maintains a Neutral rating. Oppenheimer cut to $16.

On April 2, 2026 — two months after Tremont closed — Blue Owl capped redemptions on two of its largest retail-facing credit funds. Blue Owl Credit Income Corp (OCIC), a $36 billion BDC, had received requests to redeem 21.9 percent of shares in the first quarter, up from 5.2 percent the prior quarter. Blue Owl Technology Income Corp (OTIC) saw 40.7 percent of shares requested for redemption, up from 15.4 percent. The firm limited redemptions to 5 percent per quarter at both funds. In its investor letters, Blue Owl cited “heightened market concerns around AI-related disruption to software companies” as the driver. The stock dropped 8 percent the same day.

In February 2026, Bloomberg reported that co-CEOs Doug Ostrover and Marc Lipschultz had each pledged more than 130 million Blue Owl shares — roughly two-thirds of their personal stakes, representing approximately $1.1 billion in combined collateral — for undisclosed personal loans. As the stock fell, the collateral weakened. On April 17, 2026, Blue Owl filed an 8-K disclosing that the executives had removed all firm shares as loan collateral. The Wall Street Journal and Bloomberg both reported the change was driven by concerns about imminent margin calls.

A federal securities fraud class action sits in the Southern District of New York. Goldman v. Blue Owl Capital Inc., 25-cv-10047, filed in December 2025 by Robbins Geller Rudman & Dowd, ranked the top securities class action firm by recovery in four of the last five years, names a class period of February 6 through November 16, 2025. The complaint alleges that Blue Owl failed to disclose to investors that it was experiencing meaningful pressure on its asset base from BDC redemptions; that it was facing undisclosed liquidity issues; that it would likely need to limit or halt redemptions; and that its positive public statements about its business and prospects were, therefore, materially misleading.

Set those facts on a single timeline.

December 2024: Big Lots vacates Tremont. Blue Owl’s net-lease fund holds a stranded 1.3-million-square-foot warehouse with no tenant.

February – November 2025: The alleged class period. Blue Owl continues making public statements about its liquidity and prospects that investors later allege were materially misleading.

July 2025: The Navy announces WEXMAC-TITUS — the domestic detention expansion of the Afghanistan-era WEXMAC contracting vehicle.

September 2025: ICE begins awarding detention conversion contracts through WEXMAC.

December 2025: Securities fraud class action filed.

January 15, 2026: Tremont deed agreed.

January 29, 2026: Deed takes effect. Blue Owl receives $119.5 million.

February 4, 2026: Bloomberg reports the sale.

February 9, 2026: Bloomberg reveals the founders’ pledged stakes.

April 2, 2026: Blue Owl caps redemptions at OCIC and OTIC; stock drops 8 percent.

April 17, 2026: Founders remove all Blue Owl shares as loan collateral, three days before this piece is published.

Blue Owl received $119.5 million in cash for a stranded asset approximately two months before its public liquidity crisis became undeniable. The cash came at the moment when cash mattered most, to a firm whose investors were about to demand their money back, whose founders were watching their personal collateral evaporate, and which was already defending against federal allegations that it had concealed exactly this condition.

That is what makes this transaction different from the others in the program. It wasn’t just that Blue Owl made money on a bad asset. It was that the federal government paid institutional rescue prices for a vacant warehouse at the precise moment when the seller most needed rescue.

The thirty-three

A search of ProPublica’s database of Trump administration financial disclosures returns 33 results for “Blue Owl.” They span the Department of State, the Treasury, the Department of Defense, the Department of Energy, the Department of Transportation, NASA, the Office of Personnel Management, the U.S. International Development Finance Corporation, the General Services Administration, the Office of Management and Budget, USDA, the DOJ, HUD, SSA, and the White House. The list includes the President, two cabinet secretaries, a NASA administrator, a Comptroller of the Currency, a GSA General Counsel, seven ambassadors, and twenty other senior officials.

For the Tremont transaction, six of those names matter operationally.

Donald Trump, President

The President’s public financial disclosure lists Blue Owl Capital Class A common stock directly — entries for “BLUE OWL CAP INC CLASS A” and “BLUE OWL CAP INC COMCL A” appear in his filing. The filing does not itemize a dollar figure; U.S. News’s analysis of Trump’s fuller holdings estimates the position at more than $5 million. The president personally owned stock in the company that sold the Tremont warehouse to the government he runs.

John Phelan, Secretary of the Navy

Phelan’s department administers WEXMAC-TITUS. His January 2025 financial disclosure, filed ahead of his March 2025 confirmation, showed $5 million to $25 million in Blue Owl Capital Class A common stock, generating $100,000 to $1 million in annual income. It also showed founding-era Owl Rock GP carry interests through White Tip Investments LLC: two of those positions each produced “$5 million or more” in capital gains tied directly to Blue Owl appreciation, because Owl Rock was the pre-2021 predecessor of Blue Owl Capital. Phelan also held positions in two Blue Owl Healthcare Opportunities funds, one with an outstanding $15,000 to $50,000 unfunded capital call.

On June 11, 2025, the Office of Government Ethics issued Phelan a certificate of divestiture for “Blue Owl Capital Inc.” stock. A certificate of divestiture is permission to defer capital gains taxes upon sale — it is not proof of sale. In a statement dated July 25, 2025, OGE noted that Navy ethics staff “confirmed that Secretary Phelan is working on divestiture” and that his final certification of ethics agreement compliance was due July 31, 2025. The Navy announced WEXMAC-TITUS that same month.

Phelan’s actual OWL sale date — the transaction at which his Blue Owl common-stock holding converted to cash — has not been disclosed publicly, and no Form 4 or other post-transaction filing has surfaced to confirm whether the sale closed before or after WEXMAC-TITUS was announced. That gap matters: the entire period between his March 25 confirmation and his July 31 certification deadline overlapped with the months the securities fraud class action now alleges Blue Owl was concealing its liquidity crisis from investors. Until the divestiture date is on the public record, “Secretary Phelan is working on divestiture” is doing more analytic work than it should.

The certificate specifically covered the OWL common stock and “MSD Hospitality Partners LP.” It did not cover the Owl Rock GP carry positions, the Blue Owl Healthcare Opportunities II or III funds, or the $50 million-plus personal loan Phelan carries from his former employer MSD Capital LP at 3.31 percent — a 2020 obligation that remains on his balance sheet.

Senator Elizabeth Warren’s March 2025 letter to Phelan, sent ahead of his confirmation vote, identified his $50 million Dell position, his Palantir capital gains, and his Red Cell Partners defense-tech holdings. Those got attention. The Blue Owl positions did not. They were not raised at his confirmation hearing. His ethics agreement contains no specific recusal requirement for Blue Owl.

In February 2026, CNN reported and The Washington Post confirmed that Phelan was listed as a passenger on Jeffrey Epstein’s Boeing 727 for two transatlantic flights in 2006, according to manifests released in the Epstein files document dump. There is no evidence Phelan knew of Epstein’s offenses at that time; Epstein was first indicted months later. The detail matters because it situates Phelan in the same financial-network architecture this series has been mapping — a set of rooms the future Secretary of the Navy was already welcome in, decades before his confirmation.

Brendan Rogers, Assistant Secretary of the Navy for Energy, Installations, and Environment

Rogers was sworn in on December 23, 2025 — five weeks before the Tremont deed took effect. He came directly from BDT & MSD Partners, where he served as Chief Operating Officer until July 2025. BDT & MSD is the same institutional network as Phelan’s — both men arrived at Navy leadership from the merchant bank built around Michael Dell’s fortune.

His public financial disclosure lists “Blue Owl Cap Inc. (OWL)” directly in his “Other Assets and Income” section.

The ASN(EI&E) is the senior civilian official responsible for Navy and Marine Corps installations, real estate, infrastructure, and contingency bases — the portfolio that directly includes the physical infrastructure side of WEXMAC-TITUS. Rogers’s total disclosed assets are $22 million. He took office holding stock in the company whose subsidiary, six weeks later, became the largest single recipient of the program he oversees.

What Rogers has personally signed, approved, or been briefed on regarding WEXMAC-TITUS or the Tremont transaction is not publicly known. No Navy release, FOIA disclosure, or congressional testimony has addressed his direct role in the program. It is also not publicly known whether Rogers has recused from WEXMAC-TITUS matters, from Blue Owl matters specifically, or from neither. The question has not been asked.

Jonathan Gould, Comptroller of the Currency

Gould’s disclosure includes a line item: “BCS43-Blue Owl RE NLP Fund P LP.” NLP is Blue Owl’s shorthand for Net Lease Property. The ticker-like “BCS43” prefix and “P LP” suffix — consistent with Blue Owl’s internal convention for the private limited-partnership vehicle in its Real Estate Net Lease Property Fund family — indicate that Gould holds the same fund vehicle, or a feeder into it, that executed the Tremont sale. (Blue Owl operates both a private LP and a non-traded REIT, ORENT, under the Net Lease Property branding; Gould’s disclosure reflects the private LP.) His position: $250,000 to $500,000.

Gould’s agency, the OCC, regulates all national banks and federal savings associations — including Deutsche Bank USA (whose parent sold the Salt Lake City ICE warehouse to DHS for $145.4 million, 49 percent above assessed value) and Goldman Sachs Bank USA (whose parent is itself a separate seller-counterparty in the WEXMAC-TITUS program). Gould is the federal regulator with primary supervisory authority over the banking subsidiaries of two firms operating on the sell side of the same procurement vehicle that, in January 2026, rescued the Blue Owl fund in which he held a quarter-million-dollar position.

John Russell McGranahan, General Counsel, General Services Administration (through November 2025)

McGranahan sold his Blue Owl Capital Inc. position on January 23, 2025 — day three of the Trump administration. The GSA is the federal real estate arm whose Facilities Management Division would, in the ordinary course, administer federal property acquisitions. For the eleven warehouses in the WEXMAC-TITUS program, that ordinary course was bypassed: the contracting vehicle was Navy, not GSA. McGranahan’s office nonetheless provided legal oversight of GSA’s residual role from WEXMAC-TITUS activation in July 2025 through his departure in November.

He recognized the Blue Owl conflict, divested on day three, and then administered the procurement architecture through which Blue Owl later received $119.5 million.

Somers Farkas, Ambassador to Malta — and the Middle Tier

Farkas holds $500,000 to $1 million in Blue Owl Capital Class A common stock. Her ambassadorial role has no nexus to procurement or detention policy.

She belongs in the count not because her role matters but because she represents the middle tier of the network: not a decision-maker, not a Cabinet secretary, but a confirmed Senate appointee holding meaningful direct equity in the firm sitting on the other side of an active federal real estate transaction. The middle tier is full of Somers Farkases. The point of the network is not that any one appointee could have stopped the Tremont sale. The point is that no one in the network had any incentive to.

The remaining twenty-seven include David Eisner (Counselor to the Treasury Secretary, unfunded capital call on Blue Owl Asset Special Opportunities Fund IX), Sean Duffy (Secretary of Transportation, divested OWL February 13, 2025), Christopher Wright (Secretary of Energy, divested OWL February 27, 2025), Jared Isaacman (NASA Administrator, holds Blue Owl Capital Corporation), Scott Kupor (OPM Director, holds OWL), Benjamin Black (CEO, U.S. International Development Finance Corporation, holds OWL), Thomas Barrack (Ambassador to Turkey, holds Blue Owl Capital Corp), and sixteen others across thirteen agencies.

Reconstructing who still held what on January 29, 2026 requires filings many of these officials are not required to make public. Divestitures of publicly traded stock show up on Form 4 or subsequent ethics disclosures; divestitures of fund positions, carry interests, and limited-partnership stakes frequently do not. From what is in the public record: at least seven of the thirty-three disclosed ongoing Blue Owl exposure in filings dated after their confirmation (Rogers, Gould, Eisner, Isaacman, Kupor, Black, Barrack, Farkas — and this is a floor, not a ceiling). At least four confirmed divestitures on the public record (Duffy, Wright, McGranahan, and — subject to the unresolved date question above — Phelan’s OWL common stock). The remaining twenty-two are not resolvable from public filings alone. If the reader wants a defensible minimum: at the moment the Tremont deed took effect, no fewer than seven Senate-confirmed Trump administration officials, spanning Cabinet and sub-Cabinet roles, still held direct or indirect Blue Owl positions. The true number is almost certainly higher.

The decisions they made individually — to sell or to keep — did not add up to a collective constraint that would have prevented the Tremont transaction. Phelan received his certificate of divestiture before WEXMAC-TITUS was announced, but only for the OWL common stock, not for his other Blue Owl exposure. Rogers took office holding OWL directly, five weeks before the deed closed. Gould holds the specific fund vehicle. McGranahan divested the stock and then administered the program.

The conflict wasn’t one person’s. The conflict was the network. It persisted through personnel turnover because the network was the point.

The eyes and the cages

Blue Owl is not only a real estate firm offloading distressed warehouse assets.

In May 2025, the firm closed Blue Owl Digital Infrastructure Fund III at $7 billion — nearly double its $4 billion target, focused on hyperscale AI data centers for the largest technology companies in the world. Its digital infrastructure strategy has now raised $34 billion across 90-plus facilities in 25-plus markets.

In October 2025, Meta Platforms and Blue Owl formed a $27 billion joint venture to develop the Hyperion AI data center in Richland Parish, Louisiana.

The same balance sheet that is building the hyperscale infrastructure for the AI systems used to identify, track, and flag people for enforcement was the balance sheet holding a vacant 1.3-million-square-foot warehouse in Tremont Township, waiting for the federal government to take it off its hands at double market value.

Meta’s enforcement-adjacent footprint is not hypothetical, though the relationship is messier than a single-vendor story. Clearview AI built its facial-recognition database partly by scraping images from Meta’s platforms — a practice Meta sought to stop, sending a cease-and-desist letter in February 2020 and later supporting private-party and regulatory actions that produced, in 2025, a $51.75 million class-action settlement and a 23 percent equity stake in Clearview for plaintiffs. Meta’s targeted-advertising infrastructure has, separately, been used by federal enforcement agencies and their contractors for audience-building and messaging campaigns. The computing capacity that Hyperion is being built to provide — the same capacity Blue Owl’s $27 billion co-investment is underwriting — is the substrate on which the next generation of enforcement-AI will sit, whether Meta chooses to host it directly or not.

Blue Owl’s digital infrastructure portfolio hosts workloads for AWS, Microsoft Azure, and Google Cloud — the three hyperscalers that collectively carry the majority of federal cloud-based enforcement and surveillance computing under the Joint Warfighting Cloud Capability contract and its predecessors. The vacant warehouse in Tremont and the hyperscale data center in Richland Parish are line items on the same firm’s balance sheet.

The eyes and the cages. The same balance sheet carries both.

The architecture, made visible

The series that includes this piece has now documented five variations of the same capture.

The Blueprint, from Bradford County, Florida, showed the local sheriff-led operating model — a former ICE acting director’s consulting firm pitching a 3,000-bed “detention campus” designed, in its own words, to avoid “an outward presentation that advertises the campus as a detention facility.”

The Bypass showed the procurement mechanism — a Navy logistics contract vehicle originally designed for forward operating bases in Afghanistan, repurposed for domestic warehouse purchases, with a GSA Administrator who came from Goldman Sachs and held millions in the firm selling buildings through the door he left unlocked.

The Lutnick System showed the family network — a Commerce Secretary whose sons run the firms that broker tariffs, refinance detention warehouses, and finance the family’s ownership structure through a cryptocurrency company under DOJ investigation.

The Sharkov System showed the foreign counterparty with a domestic escape valve — a Russia-founded developer that once printed chocolate bars with Vladimir Putin’s face, lost its Georgia detention deal to local water infrastructure limits, and is now trying to pivot the same vacant warehouses into AI data centers.

The Blue Owl System is the fifth: a taxpayer rescue of a distressed private credit firm, executed through the same WEXMAC-TITUS vehicle, on behalf of a beneficiary in which thirty-three Trump administration officials — including the President, the Secretary of the Navy, and the Assistant Secretary of the Navy responsible for installations — held direct or indirect positions.

The overpayment is not what makes this piece different from the others. Every warehouse in the program was overpriced. What makes this piece different is the condition of the counterparty at the moment of transaction: a firm whose investors were demanding their money back, whose founders’ personal collateral was eroding, whose public filings were being challenged in federal securities litigation, and which was holding a stranded asset that had just lost its only tenant to bankruptcy. Into that acute pressure came a $119.5 million check from a program administered by officials who held its stock.

The Congressional response has been partial. Senators Warren and Shaheen wrote to Defense Secretary Hegseth in March demanding an end to WEXMAC-TITUS for domestic detention construction. The DHS Inspector General opened a formal investigation on March 26 into non-competitive contracts awarded during fiscal year 2025. Senators Warren and Raskin, joined by fifty-two colleagues, sent investigation letters to six detention contractors. The contractor response deadline was April 13. The contractor list did not include Blue Owl.

The question that has not yet been asked, publicly, of any of the thirty-three is the one that would matter most: what did you know about the planned Tremont transaction, and when did you know it? The securities fraud class period includes the months when Blue Owl is alleged to have concealed its liquidity crisis from investors. If government officials holding its funds had material non-public knowledge of a planned $119.5 million transaction at double market value during that same period, the question is not academic.

It is the question the class action was written to ask.

If you have information about Blue Owl Capital, WEXMAC-TITUS procurement, or federal warehouse purchases in your community, contact me securely.

This investigation connects to The RAMM’s ongoing documentation of the detention infrastructure. The detention expansion is tracked in the Capture Cascade Timeline.

Subscribe

Sources

The transaction

Citizen Standard: Commissioner Hess confirms $59.6M assessment (Feb 10, 2026)

Bloomberg: Blue Owl fund sells to DHS for ICE mega jail (Feb 4, 2026)

The Real Deal: Blue Owl sells Pennsylvania warehouse to ICE for $120M (Feb 5, 2026)

Chain of title

Financial distress

Bloomberg: Blue Owl BDCs impose caps after 41%/22% redemption requests (April 2, 2026)

Bloomberg: Co-CEOs’ personal loans no longer backed by firm shares (April 17, 2026)

Bloomberg: Founders pledged $1.9B stake before stock plunge (Feb 9, 2026)

Robbins Geller: Goldman v. Blue Owl Capital Inc., 25-cv-10047

CNBC: Blue Owl caps private credit funds redemptions at 5% (April 2, 2026)

Durant counterfactual

NonDoc: Durant and Choctaw Nation oppose ICE facility (Jan 14, 2026)

Project Salt Box: Choctaw Nation buys former Big Lots warehouse

Financial disclosures

Phelan and Epstein

CNN: Navy Secretary John Phelan on Epstein’s plane in 2006 (Feb 6, 2026)

Washington Post: Phelan appears in Epstein files (Feb 7, 2026)

Navy Times: Phelan reportedly listed in Epstein flight manifest (Feb 6, 2026)

Congressional and regulatory

Warren/Shaheen letter to Hegseth on WEXMAC-TITUS (March 22, 2026)

House Judiciary Dems: Warren/Raskin contractor investigation (March 30, 2026)

Infrastructure context

Blue Owl: Digital Infrastructure Fund III closes at $7B (May 2025)

More Perfect Union: The World’s Biggest Banks May Be Benefiting (April 7, 2026)

CoStar: Sellers cash in on ICE’s revamp of detention network

Related RAMM coverage

Also, Dina Powell McCormick's Meta (PA Senator McCormick's wife) is deeply invested in Blue Owl now that it announced a $27B Hyperion partnership back in October.